Each year, more than 300,000 inheritances are declared in France, generating over €15 billion in succession taxes for the French state. With rates reaching up to 60% for distant relatives or unmarried partners, inheritance and succession planning is not just a legal formality, it’s a financial necessity. For British nationals who live in France or own a second home there, understanding how French inheritance law applies is essential to avoid costly surprises and ensure loved ones actually receive what you intend to leave them.

France’s inheritance system differs sharply from that of the UK: forced heirship rules limit how freely you can distribute your assets, and inheritance tax is applied to each beneficiary individually, not to the estate as a whole. Without proper planning, families can face delays, disputes, and a significant tax bill.

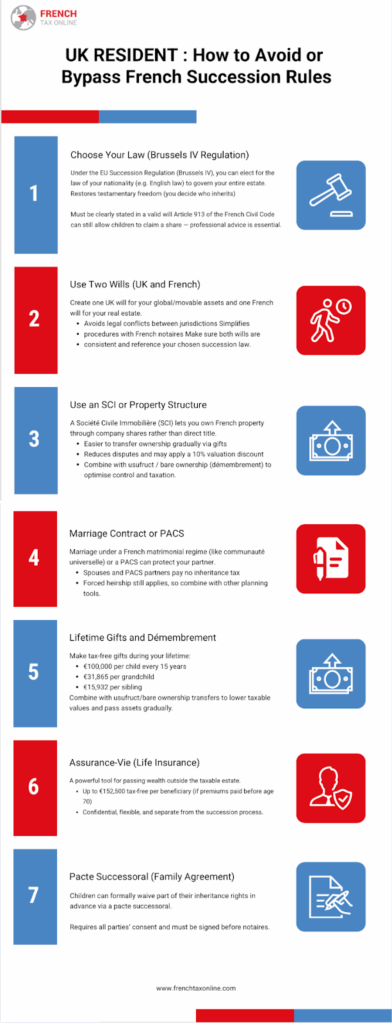

Fortunately, there are legal and efficient ways to structure your estate, from creating an SCI or assurance-vie policy, to making lifetime gifts or adopting a tailored will under the EU Succession Regulation (Brussels IV). Each tool offers a way to protect your family and reduce tax exposure.

When UK Citizens Are Affected

Whether you live in France or simply own property there, French inheritance law can apply to part or all of your estate. The key factor is not nationality, but the location of your assets and, in some cases, your tax residency.

If you are a UK citizen living permanently in France, French inheritance rules (droit de succession) apply to your entire worldwide estate, including property, bank accounts, and investments held abroad. Your heirs will therefore be taxed according to French inheritance law and rates, even for non-French assets, unless a double taxation treaty applies.

If you are non-resident in France but own French property (such as a second home or rental investment), only your French assets are subject to French succession law and inheritance tax. Your other assets outside France remain governed by UK law.

It is also important to note that French civil law automatically governs French real estate, regardless of the owner’s nationality or will, unless a specific election under the EU Succession Regulation (Brussels IV) has been made to apply UK law instead.

In short:

- Residents of France: French law applies to all worldwide assets.

- Non-residents with property in France: French law applies only to French assets.

- UK citizens with both UK and French assets: will face mixed rules, requiring careful estate planning to avoid conflicts and double taxation.

To avoid unexpected tax exposure and ensure your estate passes according to your wishes, it’s crucial to plan ahead with cross-border legal advice, something our team at French Tax Online specialises in.

Estate Planning Options

When living in France or owning property there, estate planning is crucial to protect your assets, reduce taxes, and ensure your wishes are respected. Several legal options allow you to structure your estate efficiently and limit the impact of French inheritance law.

One of the most popular solutions is the Société Civile Immobilière (SCI), which allows you to own property through a company rather than directly. This structure simplifies the transfer of property between family members, avoids disputes in joint ownership, and can even reduce the taxable value of the estate through a valuation discount. It offers both flexibility and control for couples and families.

The assurance-vie, or French life insurance, is another cornerstone of estate planning. It enables you to transfer wealth outside the taxable estate, with each beneficiary enjoying a tax-free allowance of up to €152,500 if contributions were made before age 70. It provides liquidity, confidentiality, and flexibility, making it particularly useful for cross-border families.

For couples, adopting a French marriage contract or entering into a PACS can strengthen legal and fiscal protection. Spouses and PACS partners are fully exempt from inheritance tax, and certain regimes, such as communauté universelle, allow assets to pass automatically to the surviving partner.

You can also make lifetime gifts (donations) to reduce future inheritance tax. France offers generous tax-free allowances, €100,000 per child and €31,865 per grandchild, renewable every 15 years. Combined with démembrement de propriété (splitting ownership between usufruct and bare ownership), this allows parents to retain use of the property while progressively transferring it to their heirs.

The EU Succession Regulation (Brussels IV) allows British nationals to elect for English law to govern their French estate. This restores testamentary freedom and lets you decide who inherits, although the election must be clearly stated in your will and coordinated with French notarial rules.

Infographic : How to Avoid or Bypass French Succession Rules

Overview of French Inheritance Law

French inheritance law, or droit de succession, is based on the principle of forced heirship, meaning that part of your assets must go to specific family members, mainly your children. This contrasts sharply with UK inheritance law, which allows full freedom to decide who receives your wealth.

Under French law, children are protected heirs (héritiers réservataires). They are legally entitled to a fixed share of your inheritance, called the reserved portion (réserve héréditaire). The remaining share, known as the freely disposable portion (quotité disponible), can be given to anyone you choose.

Here’s how the inheritance is divided under standard French rules:

- 1 child → must receive 50% of the assets.

- 2 children → must share two-thirds (66.6%).

- 3 or more children → must share three-quarters (75%).

If there are no children, the surviving spouse becomes a protected heir and is entitled to 25% in full ownership, while the rest can be distributed freely through a will.

Unlike in the UK, where your will governs everything, a French notaire must handle the legal and tax process after death, ensuring compliance with French succession rules.

In practice, this means:

- You cannot completely disinherit your children.

- Your spouse or partner may not automatically inherit everything unless specific arrangements are made.

- Any property located in France will follow French inheritance rules, even if your will was drafted in the UK.

Because of these restrictions, many British nationals in France use inheritance planning tools, such as assurance-vie, marriage contracts, or an SCI, to increase flexibility and protect their family.

Do UK wills apply to French property?

A UK will can apply to your French assets only if you have explicitly chosen for English or Welsh law to govern your inheritance under the EU Succession Regulation (Brussels IV). Without this election, French inheritance law automatically applies to any property located in France, including second homes or investments. It is strongly advised to make a separate French will for your French property and ensure it aligns with your UK will.

Can I disinherit my children under French law?

Generally, no – but there is an important international exception.

Under French inheritance law, children are protected by forced heirship rules (réserve héréditaire). They must receive a minimum share of the estate:

- 50% with one child

- 66.6% with two

- 75% with three or more

Only the remaining portion (quotité disponible) can normally be left freely.

However, under the EU Succession Regulation (Brussels IV), a person living in France but holding the nationality of another country may choose the law of their nationality to govern their estate. In many countries, inheritance law does not impose forced heirship, which may make it legally possible to exclude children – subject to strict conditions and current French case law.

The experts at French Tax Online provide tailored international estate planning to help you structure your will correctly and protect your family’s future.