As part of the exercise of your activity, whether you are under the LMNP or LMP status, you will have to pay several taxes.

Some taxes are inherent to both statuses, while others will apply to only one status.

In the following paragraphs, therefore, we will distinguish between those that apply to these two regimes and those whose index relates to one or the other.

Taxes for both LMNP and LMP

Taxes for the benefit of territorial collectivities:

In LMNP, these taxes are deductible from rental income if you have chosen the régime reel simplifié to declare your income.

- Taxe foncière: this is a local property tax, due every year by the owner of the property or the usufructuary of the furnished accommodation. It is calculated according to the rental value established by the local authority. It is not recoverable from the tenant.

- The Contribution Foncière des Entreprises (CFE): the CFE is a local tax intended to replace the professional tax. LMNP are liable for this each year, in november/december, whether they are taxed under the micro-BIC regime or the régime réel.

- Tax on Vacant Housing (TLV): the tax on vacant housing can be claimed from the owner who has vacant properties for residential use. This must have been vacant for at least one year as of January 1 of the tax year. Only dwellings located in certain municipalities are concerned (belonging to a continuous urbanization zone of more than 50,000 inhabitants). You may be exempt from the TLV if during the reference year the accommodation is occupied for more than 90 consecutive days. You can prove this occupation using your rental income statement, your electricity receipts etc. Another case of exemption is the involuntary vacancy of the property: if you cannot find a tenant, for example.

Furnished second homes subject to housing tax (taxe d’habitation) are also not affected by this tax.

Social security contributions:

In France, when you generate income, you are subject to social security contributions.

This rate applies to net income, which is to say:

- Net revenue abatement if you are under the flat-rate scheme

or

- Revenue net of charges if you are on a régime réel.

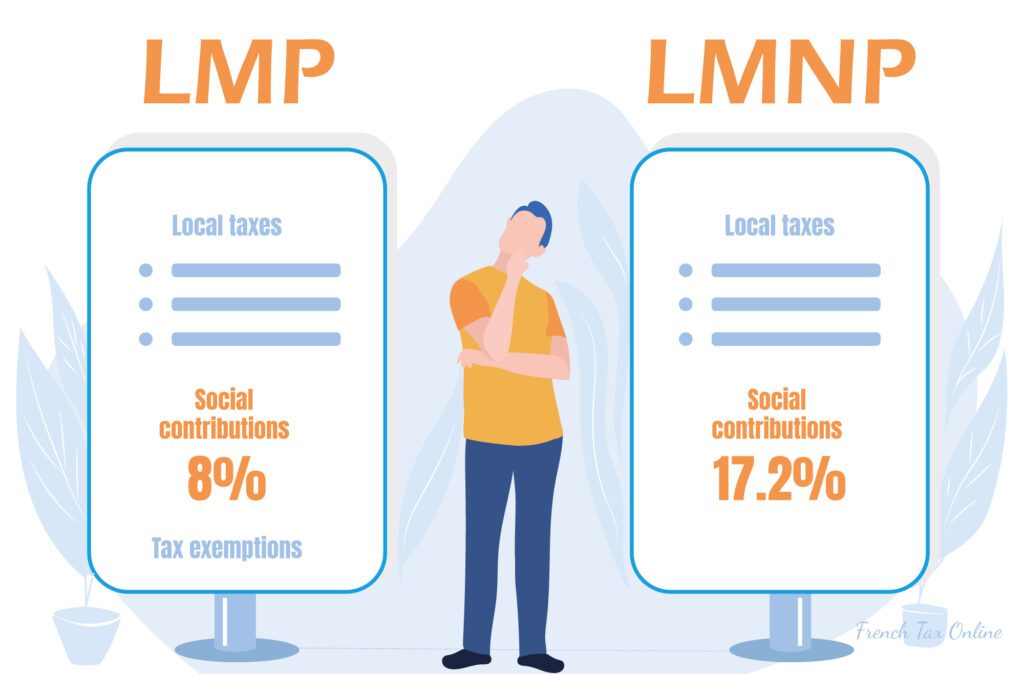

Under LMNP status: régime des revenus du capital– social security contributions represent 17.2% of your taxable income and are as follows:

| Contributions : régime des revenus du capital | Rate |

| Contribution sociale généralisée (CSG) | 9.2% |

| Contribution au remboursement de la dette (CRDS) | 0,5% |

| Prélèvement de solidarité | 7.5% |

- Under LMP status- régimes des revenus d’activité : social security contributions represent 8% of taxable income and break down as below:

| Contributions : régimes des revenus d’activité | Taux |

| Contribution sociale généralisée (CSG) | 7,5% |

| Contribution au remboursement de la dette (CRDS) | 0,5% |

The LMP related taxes

- Real estate capital gain: provided that the activity has been carried out for at least five years, you benefit from a total exemption from professional real estate capital gains if your rental income is less than 90,000€ per year. The exemption is partial from 90,000 to 126,000 €. Capital gains are taxed at a rate of 12.8% + 17.2 (or 7.5%) social contributions.

- Wealth tax (IFI): you escape from the real estate wealth tax, which replaces the ISF since 2018, legally if your income exceeds € 23,000 per year AND if the net income minus charges and depreciations represent more than 50% of the income of the household.

- Passed on patrimony: you pass on the patrimony under excellent conditions thanks to a preferential tax regime on inheritance rights.

Want to learn more about capital gains taxation in LMNP?

Although the exemption rules differ under LMP, capital gains in LMNP are also subject to specific tax rules depending on how long the property has been owned.

Check out our dedicated article on LMNP capital gains taxation